Federal IT Busy Season – Countdown to Contracts or Cuts?

Published: July 24, 2013

The last two months of fiscal year (FY) 2013 are upon us and normally that would mean that the “federal IT busy season” is heating up. But will sequestration, continuing resolutions, furloughs, and program delays mean a radically subdued busy season? Let’s see.

Last week, I looked at total contract obligations covering all procurement categories with a view that we could see about $230 billion if overall contracted spending in Q4. This week I want to narrow the consideration to just information technology (IT.)

The historical trend of an increasing proportion of IT obligations shifting into the fourth quarter is well established. Over the last 5 years the trend has been almost perfectly consistent as continuing resolutions have delayed contracts farther into the year. In FY 2011 and FY 2012 the percentage of IT dollars that were obligated in Q4 were 43% and 40% respectively. (See chart below.)

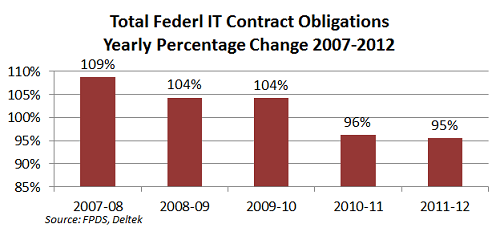

What might this mean for Q4 of FY 2013 for IT? Let’s see what we can infer from the data and draw some conclusions. If we compare the year-to-year percentage change in IT obligations over the previous 5 fiscal years we see that the yearly percentage growth has decreased since 2007 with FY 2011 and FY 2012 each recording 4-5% less than the previous year. Even with the current pressures to reduce spending, it seems that the real turn came in FY 2011 when we saw year-over-year reductions begin. (See chart below.)

In FY 2012 there were over $73.7 billion in IT obligations reported, which was 95.5% of what was reported in FY 2011. Given the recent downward trend and the widely-held expectation that this trend will continue . . . simply applying that 95.5% rate from 2011-12 to the $73.7 billion from FY 2012 would give us about $70.4 billion for estimated total FY 2013 IT obligations. (See chart below.)

If we apply the same proportion of Q4 spend as in FY 2012, assuming that the historical shift trend continues, this means that Q4 spending on IT could come in at around $28 billion for FY 2013. This level would fit perfectly with recent historical spending, even when accounting for some belt-tightening at agencies.

Under this scenario, even if we do see an overall reduction from last year, we are not talking about radical reductions. Yes, it will to make busy season more competitive, but it shows that there is still a huge market opportunity to pursue . . . especially over the next few weeks.