IT Market Forecast Finds Bright Spot in Cloud

Published: July 10, 2013

Cloud ComputingContract AwardsCybersecurityForecasts and SpendingGeospatialMobilityOMB

The latest forecast from Deltek’s Federal Industry Analysis Team predicts a slight decline in total IT spending over the next five years, from $112 billion in FY2013 to $102 billion in FY 2018. The flat to slightly lower spending levels reflect the demands of the federal budget environment, which is driving efforts to increase efficiency and effectiveness of IT investments while bringing increased scrutiny. While this reality has been characterized in the near term by phrases like “do more with less” and “flat is the new up,” government organizations are continuing to spend billions of dollars in contracts for IT products and services. The shift to cloud services is enabling agencies to achieve increased capabilities, like security and mobility, without the burden of traditional implementation and maintenance costs. With the value cloud contract awards nearly quadrupling between FY 2012 and FY 2013, it’s hardly surprising that this area will continue to see investment over the next five years.

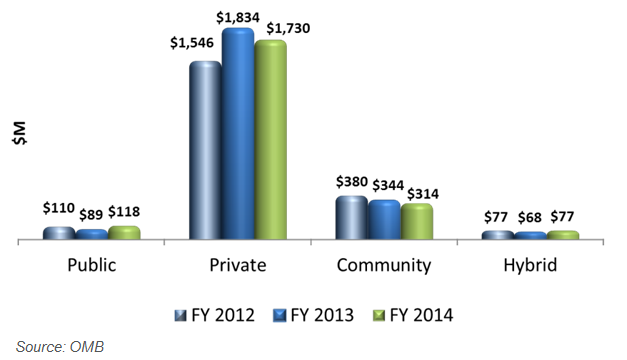

A new feature in this year’s budget reporting required agencies to publish spending related to cloud computing, including funds required for implementation (hardware, software, professional services) in addition to the cloud service itself. Over the past few years, government spending on cloud computing has favored private deployments. While the reported figures appear to reflect a decline from FY 2013 to FY 2014, we expect to see those numbers for private clouds to increase, although new budget realities may slow the pace.

While cloud service provider authorizations have been slowly doled out through the Federal Risk and Authorization Management Program (FedRAMP) office, agencies have pursued cloud procurement through a variety of channels – including government-wide acquisition contracts (GWAC), set asides, sole sourced awards, and GSA schedules. Even as adoption of cloud computing has gained momentum, agencies have remained hesitant about mission critical applications. As cloud providers build trust providing current service offerings, these untapped mission-critical areas may be primed for efficiency improvements and cloud service expansion. Maturation of cloud adoption also stands to support business system transformation, potentially through a shared services model. Trends across defense and civilian agencies that will sustain investments in cloud computing over the forecast period include:

Defense

- While most services are pursuing solutions through DISA, the approach is not uniform.

- Demand for support of storage, cyber security, and intelligence, surveillance and reconnaissance (ISR) analysis.

- Implementation of common computing environments, service oriented architecture (SOA), and combat support systems will progress as cloud adoption matures.

Civilian

- Civilian agencies are exploring increased roles for commercial cloud services.

- Infrastructure consolidation, mobility, data management and shared services are developing in tandem with cloud efforts.

- Beyond webhosting, email and collaboration, cloud solutions are being targeted for geospatial and scientific data.

- Agencies are also turning to cloud-based mobile device management.

- System modernization based on cloud solutions is poised to be an area of high growth, particularly if providers are able to reduce latency and improve up time.

So while we foresee some decline in overall market segments during the next five years, cloud computing is one technology area anticipating continued investment and growth. As cloud gains momentum and consolidated technologies require less integration and customized service, spending in IT services is likely to soften. For more information on the IT spending forecast and specific agency outlooks for cloud computing, see Federal Information Technology Market, 2013 – 2018.