FY 2022 Improper Payment Totals Show First Decline in Over Five Years

Published: December 01, 2022

Total federal improper payments fell to $247B in FY 2022 according to data recently released on paymentaccuracy.gov. The improper payment rate also decreased from 7.2% of program outlays in FY 2021 to 5.1% in FY 2022, amounting to a $34.3B or 12.2% decline.

Improper payments (IP) are payments made by the government to the wrong person, in the wrong amount, or for the wrong reason. Improper payments include both overpayments and underpayments. Improper payments do not directly translate to fraud or monetary loss but need addressing to protect the integrity of taxpayer and federal funds.

To reduce IP in federal programs, Congress has passed several pieces of legislation since 2002. The Improper Payments Elimination and Recovery Act of 2010 (IPERA) expanded the core principles of the 2002 Improper Payments Act in the areas of agency IP identification, compliance, and reporting requirements. Additionally, OMB has been working with federal agencies to implement the Payment Integrity Information Act of 2019 to improve payment integrity.

The new data shows the first drop in improper payment totals and rates since FY 2017.

The decrease in FY 2022 IP is mostly attributable to the Federal-State Unemployment Insurance (UI) program where IP dropped dramatically from $78B in FY 2021 to $18.9B in FY 2022. Improper payments for UI surged in FY 2021 due to the pandemic, rising from only $7.9B in FY 2020. The pandemic triggered a massive surge in UI claims that overwhelmed state-run agencies responsible for administering unemployment insurance. Outdated IT systems and limited statutory fraud and eligibility controls make the UI program more susceptible to improper payments.

Although total IP for UI decreased in FY 2022, the rate of IP increased from 19% of program outlays to 22%. The increase is a direct result of persistent pandemic effects on state UI administrations which continue to endure the burden of legacy IT and were required to resume work search requirements for applicants which were waived during the pandemic.

Additionally, the Medicaid program saw a decrease in IP from $98.7B in FY 2021 to $80.6B in FY 2022 while outlays increased, equating to a drop in IP rates of more than 6%.

In an effort to reduce administrative burden and make IP data and information more useful and actionable, OMB made several changes to the payment integrity compliance framework in March 2021. One of these changes is a new categorization of payment types. Payments are now classified as proper payments, improper payments, or unknown. An “unknown” payment is defined as a payment that cannot be discerned as improper or proper. Previously, unknown payments would have been grouped with improper payments.

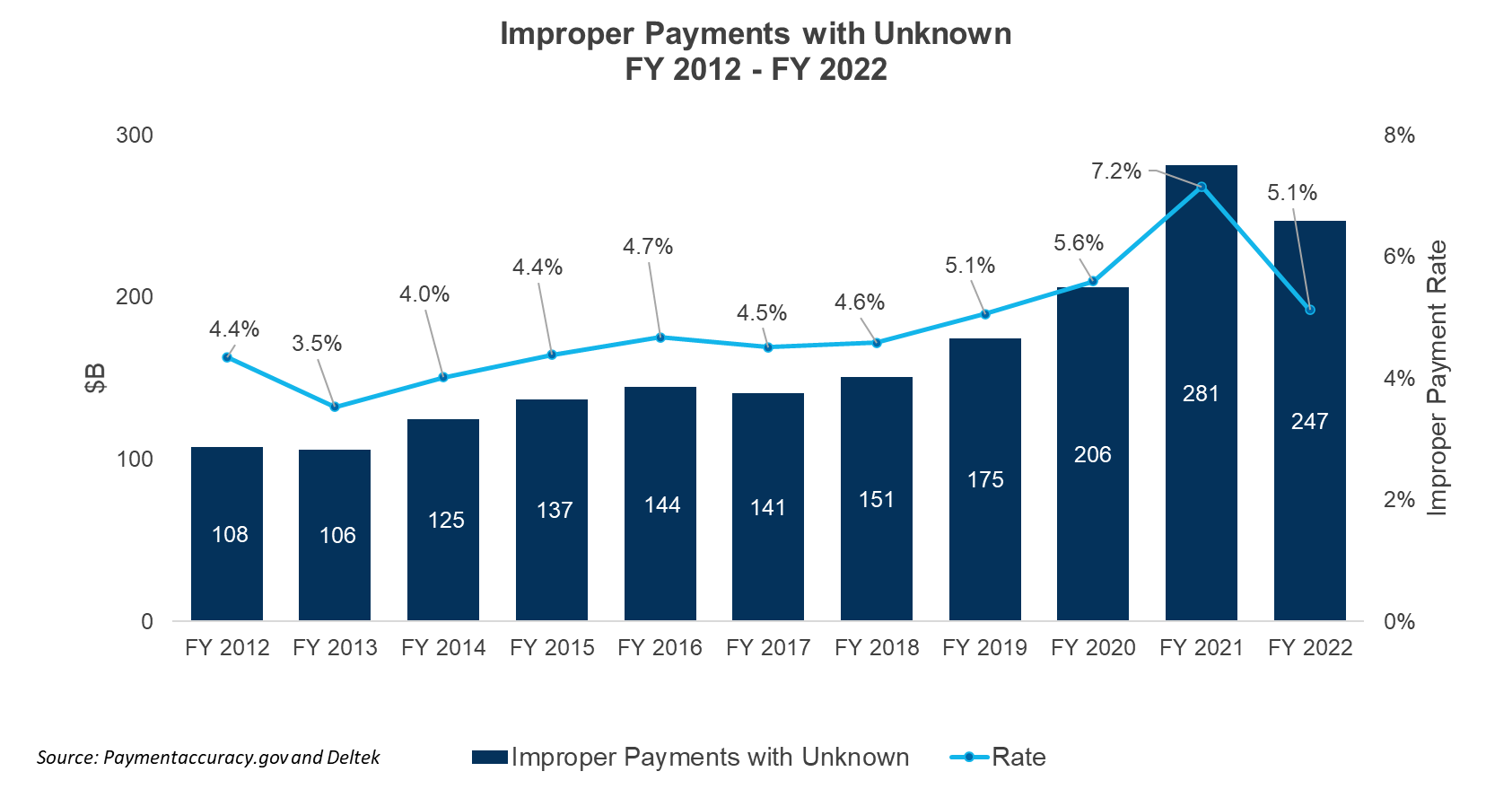

The chart below shows totals for IP without unknown payments for the last four years.

Agencies began classifying payments as unknown in FY 2019. Most of the unknown payments occurred in FY 2019 and FY 2020. In FY 2021, the IP amount with unknown payments was relatively close to the IP amount without unknown payments. However, there is more divergence between IP with and without unknown payments in the FY 2022 numbers.

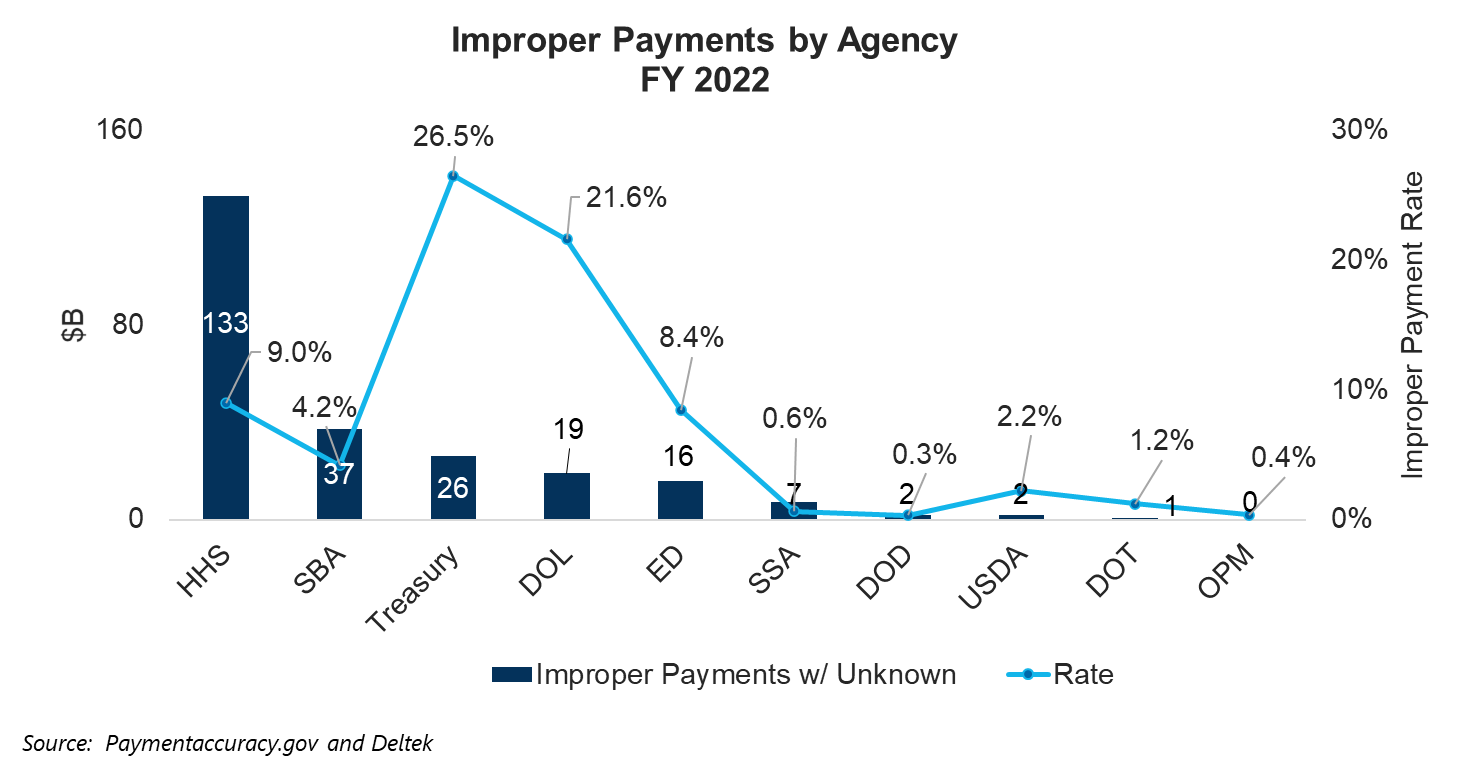

Charted below is the distribution of IP by agency for FY 2022:

HHS continues to show the highest amount of IP at $133B, equating to 9% of the agency’s total program outlays for FY 2022.

In FY 2022, Medicaid outpaced the Medicare FFS program for the largest improper payment totals at $80.6B and a rate of 15.6% of total program outlays. The Medicare FFS program shows the second largest IP amount at $31.5B with a 7.5% improper payment rate. Stemming from COVID relief funding, the Paycheck Protection Loan Program (PPP) and the COVID-Economic Injury Disaster Loan (EIDL) both out of SBA are new to the list this year, showing $29B and $6.9B in IP respectively.

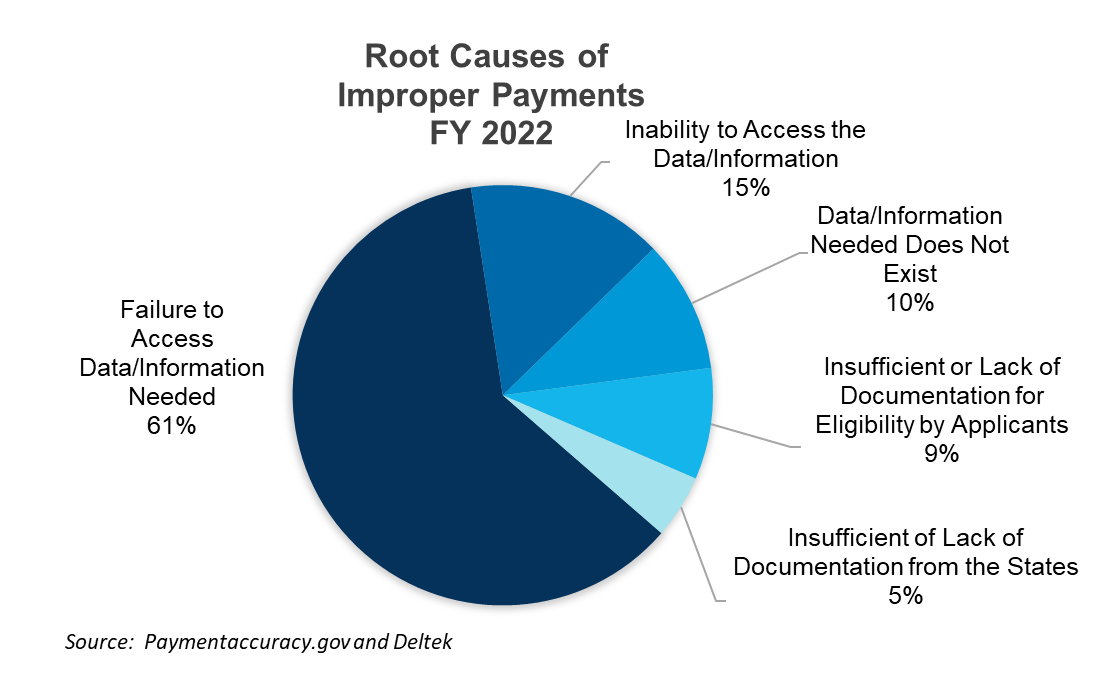

Below are the main causes for IP in FY 2022:

Most IP are due to the failure to access data or information needed to determine if a payment is improper. This occurs because of human error to access the appropriate data or information to determine whether a beneficiary or recipient should be receiving a payment, even though such information exists and is accessible to the agency or entity making the payment.

The second most frequent cause of IP is the inability to access data or information to determine if a payment is improper. In this case, the information needed to validate payment accuracy exists but the agency or entity making the payment does not have access to it.

In an OMB memo regarding the new IP totals, the agency stated that it is “partnering with agencies to drive down improper payments” while “supporting and liaising with the oversight community.” Additionally, OMB issued implementation guidance directing agencies to be effective stewards of taxpayer resources when implementing the American Rescue Plan, the Infrastructure and Investments Jobs Act, and the Inflation Reduction Act. OMB and the administration are committed to combatting payment errors and delivering effective, efficient, and accountable government.

Efforts to curb waste and IP could lead to contracting opportunities for forensic accounting, investigators, claims analysts, and IT products and services, such as analytics, AI, and blockchain solutions.