GAO Identifies Contracting Fraud Risks at Energy

Published: February 04, 2021

Federal Market AnalysisDOEWaste, Fraud, and Abuse

High volume contracting fraud risks and DOE’s inability to completely assess these risks translates to opportunities for contractors to provide the tools and services necessary to assist the agency in identifying and preempting waste, fraud and abuse.

Key Takeaways:

- The GAO outlined nine categories of contracting fraud schemes that took place at DOE from 2013 to 2019, identifying four types that DOE missed.

- Lack of comprehensive assessment and obtaining consistent information on fraud risk from contractors contribute to DOE’s weakened assessment of contracting fraud risks.

- The agency plans to reform its agency-wide risk assessment process within the next five years, including broadening its use of data analytics, opening up opportunities for contractors to assist DOE with these plans.

In FY 2019, DOE contracted 80% of its $41B budget on contracts, primarily towards the management and operation of its scientific laboratories, environmental cleanup projects and construction of facilities. A top contender in high volumes of contracted goods and services, the DOE often falls into the line of fire for contractor mismanagement and fraudulent activities.

As such, the GAO issued a report last month assessing the contracting fraud schemes and the financial and nonfinancial impacts at DOE from 2013 and 2019, all the while identifying ways for the department to improve its antifraud practices. The federal watchdog found that while DOE has taken some steps since 2017 to improve its fraud risk management activities, there is still much work left to do by the agency to improve oversight of improper payments and conduct.

Understandably so, contracting fraud poses both financial and nonfinancial impacts at Energy. Financially, the report states that DOE identified $6.66M in improper payments in FY 2018, and $14.83M in FY 2019. These figures, the GAO finds, only represent a portion of the financial impact at DOE due to barriers in stringent reporting guidelines and difficulties in detecting fraud. Nonfinancial impacts include negative government outcomes such as program failure, risk to agency reputation, a distorted market for industry, as well as environmental and human impacts.

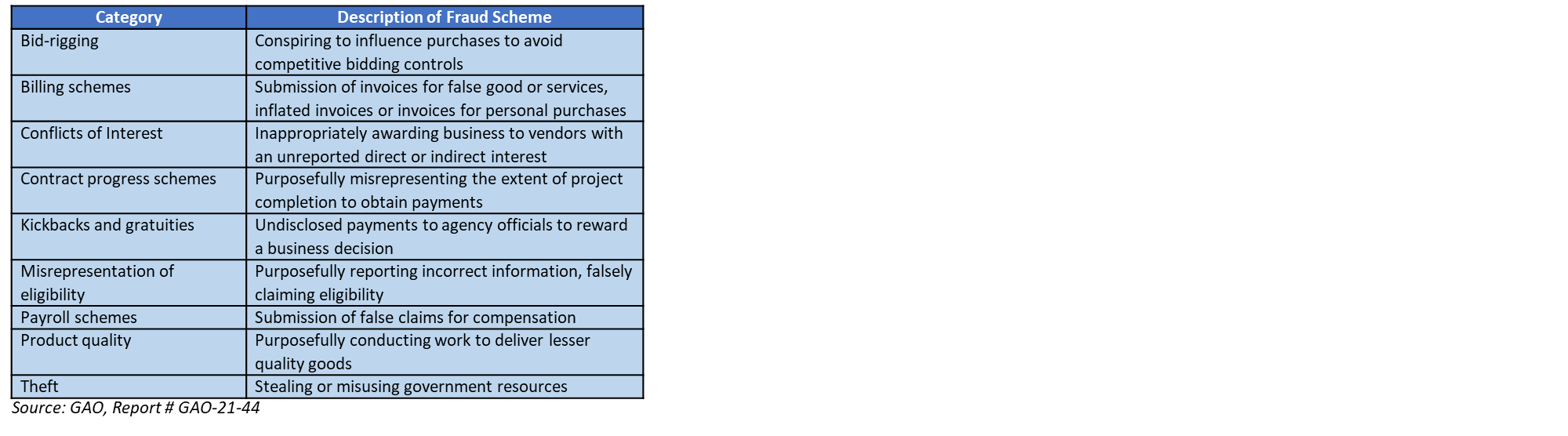

After conducting a review of publicly available information, the GAO identified the following nine types of contracting fraud schemes at the Department of Energy within the six-year span:

The GAO found that department reporting entities lacked the specificity needed in internal controls guidance to develop risk profiles of the contractors they oversee. Moreover, the government’s watchdog found that DOE has not examined “the extent to which existing control activities mitigate the likelihood and impact of inherent risks and whether the remaining risks exceed managers’ tolerance.”Ironically, the GAO identified four more contracting fraud schemes in its research than what DOE entities reported. Specifically, DOE did not identify instances of misrepresentation of eligibility, bid-rigging, kickbacks and gratuities and conflicts of interest.

The GAO found that department reporting entities lacked the specificity needed in internal controls guidance to develop risk profiles of the contractors they oversee. Moreover, the government’s watchdog found that DOE has not examined “the extent to which existing control activities mitigate the likelihood and impact of inherent risks and whether the remaining risks exceed managers’ tolerance.”Ironically, the GAO identified four more contracting fraud schemes in its research than what DOE entities reported. Specifically, DOE did not identify instances of misrepresentation of eligibility, bid-rigging, kickbacks and gratuities and conflicts of interest.

In 2017, DOE began creating a structure to oversee fraud risk management activities, including shifting all antifraud responsibilities under the OCFO to coordinate agency-wide assessments and issue internal controls guidance.

Moving forward, DOE plans to expand fraud risk assessment efforts in the next five years using a phased approach. Understanding both the gaps in the agency’s current processes and forthcoming plans will allow contractors to offer solutions and services to assist DOE during this time.

In FY 2021, the agency plans to develop an agency-wide risk assessment focused on fraud. Thereafter, DOE plans to use the new assessment toward developing an agency-wide antifraud strategy in FY 2022. The department also anticipates utilizing control activities, such as data analytics, to aid managers and employees in fraud scheme awareness, better detect potential fraud, and address emerging risks. Implementation of such control activities is slated to begin in FY 2022.