IT Spending Prospects in the Fourth Quarter of FY 2025, Part 2

Published: July 25, 2025

Federal Market AnalysisContracting TrendsForecasts and SpendingInformation TechnologySmall BusinessSpending Trends

Federal spending data points to what contractors may anticipate during this federal fourth quarter, and how they can maximize their opportunities.

Last week, I pondered the possibility that we could see $50B in IT spending in the fourth quarter of fiscal year (FY) 2025 . . . if agencies spend roughly 90% of what they spent in all of FY 2024 and made up for typical underreporting in Q3 of this year.

This week, I will take a bit of a status report on where we are at the end of Q3 and focus more deeply on monthly trends in Q4 itself. To stay consistent with my previous analysis, the data below is current through July 15, 2025.

Total IT Spending by Fiscal Quarter

Federal spending on IT grew from $120B in FY23 to nearly $127B in FY24. Three quarters through FY25, agencies remain on track to potentially meet that same level. (More on that later.) It is noteworthy that most fiscal quarters saw growth from FY23 to FY24, and Q1 and Q2 in FY25 also saw growth from FY24. Defense reporting traditionally lags by up to three months, so Q3 of FY25 is significantly underreported.

Focusing just on the Civilian segment provides a useful view. Even with quarterly fluctuations from year to year, with $31B in year-to-date FY25 obligations, the Civilian agencies are more than half-way at meeting or beating their total IT spend in FY23 and FY24. (Summary numbers include some rounding.)

Comparing the Defense and Civilian segments separately provides some perspective into the nuances of each segment, and for this I will focus on reported Q1-Q3 spending. For FY24, Defense saw a slight dip in total IT spending, but for FY25 so far, we see some significant rebounding in Q1 and Q2. As noted above, Q3 spending levels will not come into view until the DoD fully reports their contract information to the Federal Procurement Data System (FPDS).

The Civilian segment shows some a bit more consistency at the top-line level, although FY25 is currently coming in at about $1.7B below FY24. However, Civilian agencies may still have some Q3 IT obligations to report, so that Q3 total is likely to rise a bit and tighten the comparison.

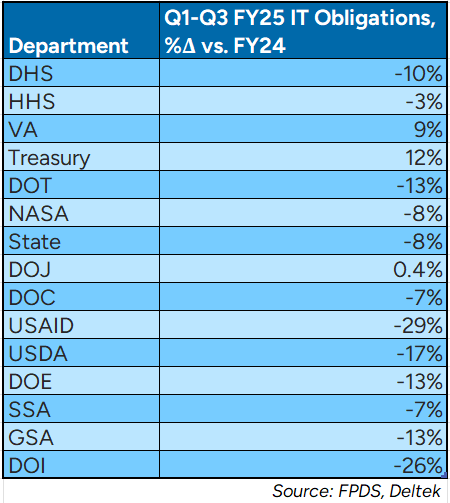

Looking into the details of Q1-Q3 FY25 spending among the Civilian department shows that only VA and Treasury are reporting increases from FY24. Justice is effectively flat. That could change if any of these departments make updates to their reported contact obligations data, which is common as the fiscal year progresses to completion.

Federal Fourth Quarter IT Spending in Focus

Focusing on Q4 spending specifically, both the Defense and Civilian segments generally follow a similar proportional pattern where roughly 50% of their Q4 IT obligations come in September. In FY 2024, we saw some spending shifts earlier in the quarter, from Aug to July, while September remained consistent from FY23.

Looking at the IT dollars spent across the federal market, including the Defense segment, FY24 saw 16% in topline growth across the market, from $41B to $48B. This occurred mostly in July and September, with August showing more modest growth from FY23 to FY24.

This strong Q4 growth in FY24 helped propel the full-year growth in FY24 to reach nearly $127B – more than $6.5B higher than FY23.

Breaking out the above data into Defense and Civilian segments provides a view of the relative proportions in total spending between the two segments.

Maximizing Opportunities in the Fourth Quarter and Beyond

There are several market drivers and inhibitors impacting the current federal IT contracting landscape of which contractor should be aware. Adapting to these, combined with following a handful of critical practices will position companies to maximize their Q4 opportunities this fiscal year.

Current drivers behind agency IT spending include leveraging IT to meet critical mission objectives, as well as the view of IT as a mission enabler and efficiency multiplier. Further, IT modernization at many agencies may be taking on a heightened priority. By some accounts, one impact of agency DOGE reviews determined that the cost and effort of maintaining legacy IT was a major source of government inefficiencies. This may drive select investments in IT infrastructure, but this may be offset by efficiency efforts in other areas of IT, such as software licensing, which may temper the impact of infrastructure spending.

On the other hand, current IT spending inhibitors include the ongoing contract scrutiny which many agencies are performing to find savings and root out inefficiencies and duplication. This is further complicated by government-wide acquisition policy initiatives, such as GSA’s OneGov strategy, which have been creating some unsettling uncertainties as these policies evolve and take shape. Further disruptions may come from organizational changes, including staff reductions and agency reorganization efforts.

Considering these uncertainties, company business development professionals need to follow some critical practices to adapt and flourish. First, assess the health of your channel up in down your supply chain to ensure that your contract performance will be up to the task when needed. Second, assess the situation at your agencies to identify changes in contracting personnel, strategies and preferred vehicles. In some cases, you may need to identify new agency champions for your solutions or contacts for existing contracting pipelines.

Bids and proposals must emphasize their alignment with current agency mission outcomes and Trump Administration priorities. (This is not limited to the current administration, but it takes on an even higher significance given the current pursuit of contracting savings and efficiencies.) Further, supply your agency program managers and contracting officers with the information they need to strongly justify their need for your offering. Suppliers may also do well to assess new pricing strategies they may need to compete in this increasingly price-sensitive atmosphere. Have these options ready in the event of any future contract reviews or renegotiations.