Reasons for Optimism in the Federal Contracting Market in 2026

Published: January 09, 2026

Federal Market AnalysisContracting TrendsForecasts and SpendingInformation TechnologyProfessional ServicesSpending Trends

Contracting data shows that fiscal year 2025 finished strong, and there are reasons for optimism in FY 2026.

The federal contracting market in fiscal year (FY) 2025 was one for the record books, filled with rapid policy initiatives and significant change that created uncertainty for many. Then, FY 2026 began with a government shutdown, adding to the turmoil. However, looking at the latest contract spending data sheds light on where the market stands, and other indicators suggest an optimistic outlook is warranted for the year.

Federal Contracting Finished Strong in FY 2025

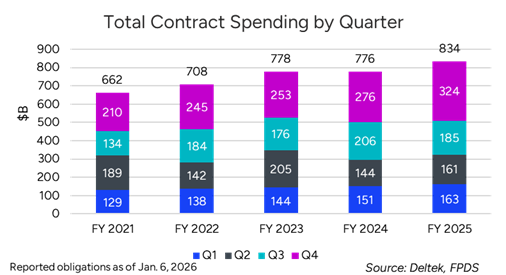

Now that we are past the customary reporting lag by the Department of Defense (DoD), which traditionally may lag up to 90 days, we can get a much clearer picture of how FY 2025 played out. Despite all the change and uncertainty that came in the year, total contract spending grew by $57.4B (+7.4%) across all areas, making FY 2025 a record year in contract spending.

Federal departments and agencies have reported $834B in total contract obligations for FY 2025, compared to $776B in FY 2024 and $778B in FY 2023. The fourth quarter of FY 2025 alone grew by more than $48.5B (+17.6%), although some of that makes up for the Q3 FY25 reduction of $21.8B compared to Q3 FY24.

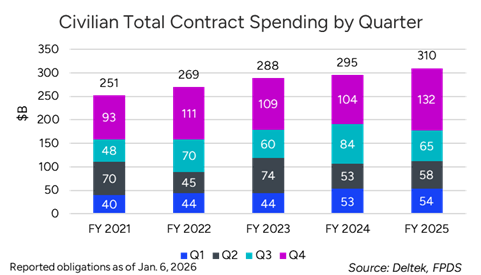

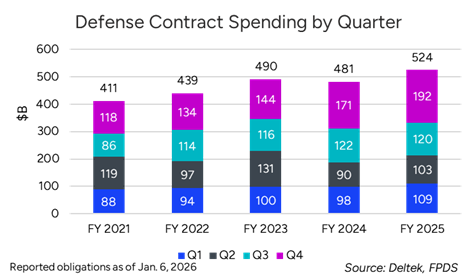

Both the Civilian and Defense sectors reported record contract spending for the year and for Q4, with both sectors overcoming some contraction in Q3.

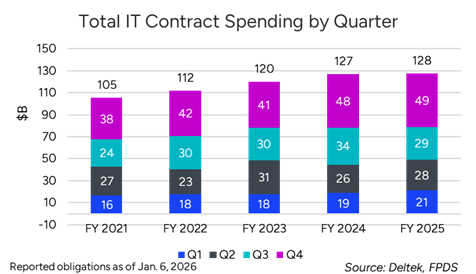

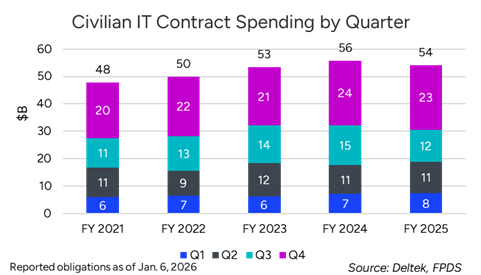

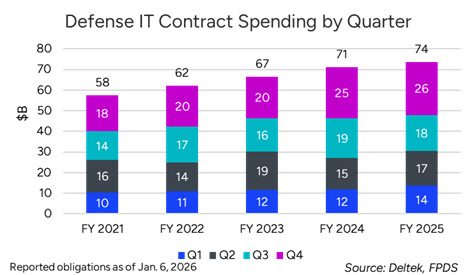

Information Technology Spending Grew in FY 2025

As Q4 FY25 got underway this summer, I speculated that we could potentially see $50B in IT spending for the quarter. Well, we got close, coming in at $49.2B in reported IT spending reported.

Civilian IT spending saw some trimming in FY 2025, but this sector still finished strongly. Defense saw another record year for IT spending, with only Q3 slightly underperforming against FY 2024.

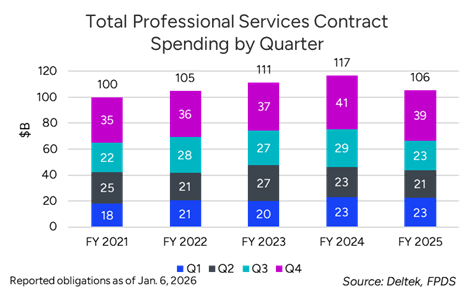

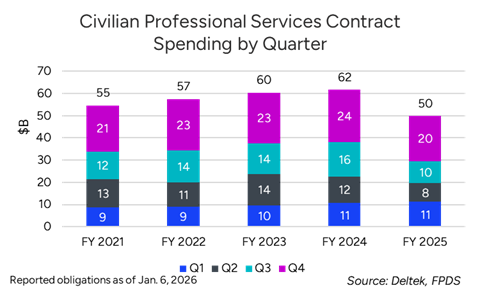

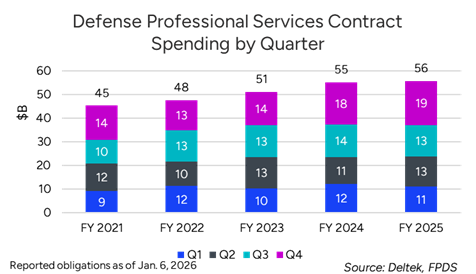

Professional Services Spending Took Hits in FY 2025

Perhaps more than any other contracting market segment, the federal professional services market has experienced some significant changes in FY 2025. Cost-cutting efforts by the Trump Administration and pressure on federal agencies to reduce their spending on professional services has taken its toll. In FY 2025, agencies reported lower PS spending in each quarter of the year, with total FY 2025 spending coming in around FY 2022 levels.

The Civilian sector took the brunt of the reductions in FY 2025, while the Defense sector came in $577M above FY 2024 levels.

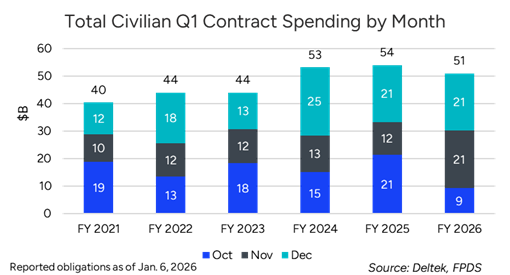

Federal Contracting is Off to a Decent Start in FY 2026

As we enter the new calendar year, should contractors be optimistic about prospects for the year? Given what we see in the data so far, the answer is a qualified yes, at least on the Civilian side, which is where we have the most complete data. Since DoD lags in their reporting by up to 90 days, we will not have a clear picture of their Q1 until later in the spring.

While Q1 FY26 is running about $3B behind FY25, much of this may be attributed to the impacts of the shutdown. October was rough, as we would expect, but November went a long way to making up lost ground.

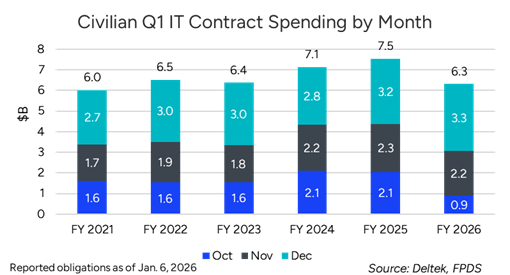

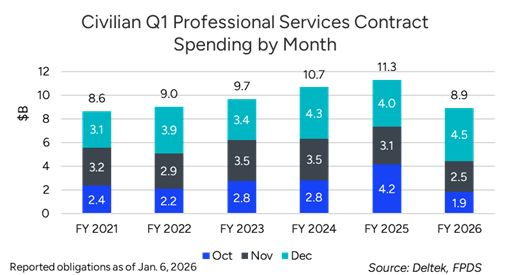

In the first quarter of FY 2026, we are seeing a similar lag in reported contract obligations across the IT and PS segments, with IT starting the year at a healthier pace than PS, as one might expect.

The reasonably quick recovery, once government operations resumed to normal, combined with the strong finish to FY 2025 supports a general outlook of optimism over pessimism for the remainder of FY 2026. Of course, the details of individual programs and procurements are where the ultimate reality resides.

FY 2026 Appropriations Will Limit Agency Budget Cuts and Restructuring

At this time, it appears that there is no interest in Congress to repeat a partial government shutdown like in October-November of last year. Even more, Congress is poised to limit any cuts to agency budgets.

Earlier this week, the House and Senate appropriations committees released details of a “minibus” of three spending bills for fiscal 2026. The three-bill package would fund the departments of Commerce, Energy, Interior and Justice, as well as the Environmental Protection Agency, NASA, National Science Foundation, the U.S. Forest Service, and other agencies.

Assuming it passes, this minibus would join the first full-year spending package that was signed in November, ending the shutdown. That bill covered three regular appropriations bills for the Department of Agriculture, the Legislative Branch, and Military Construction and Veterans Affairs, with the remaining agencies operating under a continuing resolution (CR) through January 30.

According to press release from the House Appropriations Committee, this new three-bill minibus “keeps the Committee on track to complete all 12 FY26 appropriations bills,” so it seems possible that we could see an additional minibus(s) or some combination of full-year spending bills agreed upon in time to pass before the current CR expires, meaning no shutdown and no agencies operating under a CR.

Some key aspects of the latest minibus are that it limits cuts to agency budgets from what was proposed by the Trump Administration in the FY 2026 budget proposal, and it places some limits on agency reorganization and restructuring efforts by the White House.

The Senate is scheduled to be in recess from January 19-23, and the House is scheduled for recess from January 26-30, so be on the lookout for final details on the remaining appropriations bills to take shape between now and then.

Final Thoughts

Amidst significant market change and uncertainty, the strong finish for federal contracting in FY 2025 should help bolster a more resilient perspective among market participants. Granted, we did see reduced spending in targeted areas under administration policies and initiatives. . . and it has been quite a turbulent year due to all the changes, but the market remained robust and even grew in some key areas.

The outlook for FY 2026 should remain guardedly optimistic, even with a disrupted start and some uncertainty remaining on the final disposition of many agency budgets. However, there are encouraging signs on the horizon in that regard. Yes, the market will continue to be increasingly competitive and will require contractors to stay vigilant and adaptive to change, but those that successfully navigate the changes will continue to experience market success.