Trump Administration Requires Shift from Cost+ to Fixed-Price Contracts

Published: May 01, 2026

Federal Market AnalysisAcquisition ReformContracting TrendsEOPOMBPolicy and LegislationPresident TrumpSmall BusinessSubcontracting

The new directive puts cost-plus contracts in the cross-hairs for dramatic reductions.

Yesterday afternoon, President Trump signed an Executive Order (EO) Promoting Efficiency, Accountability, and Performance In Federal Contracting, directing federal agencies to maximize their use of fixed-price and performance-based contracts, with the goal of increasing contracting savings and to drive timely and complete performance by contractors.

Motivating this latest reform action is the continued drive for cost savings in federal contracting, with the White House citing their identification of roughly $120B obligated in fiscal year (FY) 2024 on cost-reimbursement consulting contracts alone. The administration argues that these contract types provide little incentive for contractors to control costs.

The new directive puts the use of the cost-reimbursement contracts, or cost-plus (cost+), directly in the cross-hairs for dramatic reductions.

Key Elements of Promoting Efficiency, Accountability, and Performance In Federal Contracting

The latest EO and accompanying Fact Sheet address several areas of interest to federal contractors.

- Fixed-Price Contracts as the New Default. The EO establishes fixed-price contracts or performance-based contracts, tying contractor profit to performance-based metrics, as the default and preferred methods of federal procurement, replacing the prior widespread use of cost+ contracts that guaranteed contractor reimbursement regardless of efficiency.

- Approval Requirements for Exceptions. Any use of non-fixed-price contracts must be justified in writing to an agency head. Further, such written approvals are required for contracts exceeding certain dollar thresholds — ranging from $10 million for most agencies up to $100 million for the Department of Defense/War. Some exceptions exist for emergencies and research and development (R&D) on major systems.

- Mandatory Review of Existing Contracts. Within 90 days, each agency head must review their 10 largest non-fixed-price contracts by dollar value and seek to modify, restructure, or renegotiate them to incorporate fixed-price and performance-based concepts wherever practicable.

- Oversight and Implementation Timelines. Agency heads are required to submit semi-annual reports to the Office of Management and Budget (OMB) on non-fixed-price contract usage, with the first report due within 90 days. The Office of Federal Procurement Policy (OFPP) must propose amendments to the Federal Acquisition Regulation (FAR) and develop contractor training programs within 120 days.

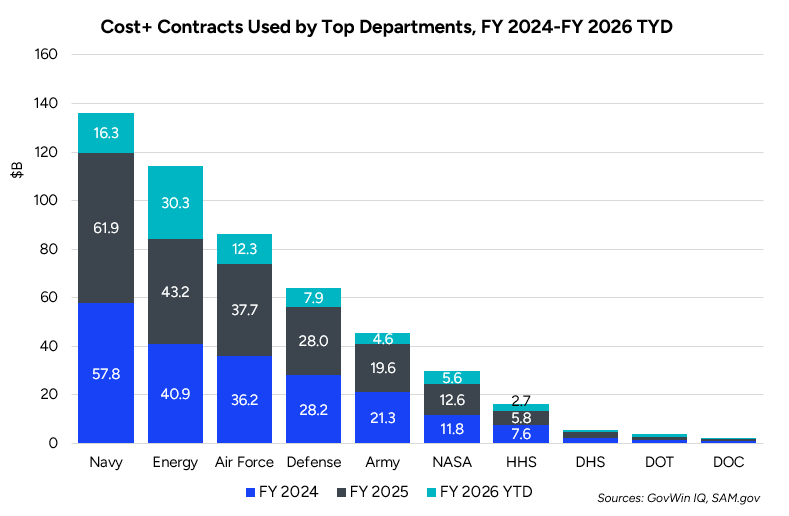

Agency Use of Cost+ Contracts

A review of reported federal contract spending data by contract type reveals that in FY 2024 and FY 2025 federal departments and agencies obligated more than $200B each year under Cost+ contracts, and more than $80B in FY 2026 year-to-date (YTD). (Note: DOD/W components can have a 90-day reporting lag, so FY 2026 data is likely understated.)

Breaking the contract spending by department shows which organizations are spending the most on Cost+ contracts over the last few years. The DOD/W components dominate the usage, but several large civilian sector departments and agencies – Energy, NASA and HHS – are among the top Cost+ users. These organizations have the most contracting dollars under scrutiny and pressure to move to fixed-price or performance-based contracts in the coming months and years.

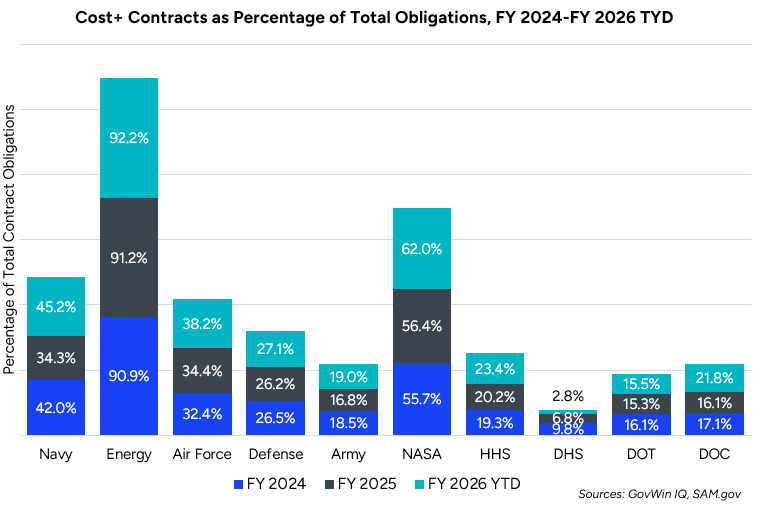

To further explore the scope of the challenge that these agencies will face in the shift away from Cost+ contracts, it is useful to look at the relative percentage that Cost+ contracts make up of their total contract spending over the last few years. Here is where a stark contrast between the DOD/W components and the civilian agencies becomes clear, with Energy and NASA obligating more than 55% of their yearly obligations under Cost+ terms.

One might well conclude that these entities may face a greater challenge in the transition to fixed price contracts. However, that will likely depend on agency leadership and the skill of their contracting staff to work through. Of course, the option exists for agency leadership to grant exceptions for emergencies and major R&D programs, so that may mediate the challenge.

Contractor Implications of the Shift to Fixed-Price Contracts

Based on provisions in the latest EO, here are some key implications for federal contractors.

- Bid & Proposal Strategy. Contractors will need to shift how they price and structure bids. Fixed-price proposals require much more precise cost estimating upfront, as there is no safety net of cost reimbursement if work runs over. This raises the stakes on proposal accuracy and will likely drive increased investment in estimating capabilities, historical cost data, and risk modeling before submitting offers.

- The Risk Profile Shifts Significantly to Contractors. Under cost-reimbursement vehicles, the government absorbed the risk for most cost overruns. Under fixed-price contracts, that risk shifts squarely to the contractor. Firms with thin margins, less mature program management, or heavy reliance on subcontractors will be more exposed to increased risk. The overall marketplace may begin to see tighter subcontract terms, greater use of contract insurance, and more conservative scope definitions as contractors try to mitigate the increased risk.

- Existing Contract Portfolios at Risk. The 90-day mandatory review of each agency's 10 largest non-fixed-price contracts means many contractors could face renegotiation of contracts that are already in progress. Mid-performance contract restructuring can be highly disruptive, especially for long-term programs. Whatever the duration, contractors should anticipate their agencies to begin initiating conversations about converting these existing non-fixed-price contracts.

- Consulting & Professional Services Firms Face Greater Impact. The EO’s explicit callout of $120B in cost-reimbursement consulting contracts in FY 2024 signals that consulting, IT services, and professional services may be a primary target of this reform. These segments have historically relied on time-and-materials (T&M) or cost-plus contracts and will likely face the greatest adjustments in both contract structure and business model.

- The Competitive Landscape Will Shift. Larger, well-capitalized contractors with strong program management offices, robust cost accounting systems, and experience in fixed-price programs will have a competitive advantage. Smaller firms and those less experienced with fixed-price work may struggle to compete or absorb risk, potentially consolidating the contractor base toward larger incumbents over time. Smaller firms may find opportunities to gain experience in these preferred contracting models through partnering with experienced large primes.

- Opportunities in Performance-Based Contracting. The EO's emphasis on linking profit to performance metrics is not inherently negative for contractors. Firms that consistently deliver on time and on budget may stand to earn higher profit margins than the Cost+ model typically allows. Contractors with strong track records at delivering on-time and within budget should highlight their past performance aggressively in proposals and position themselves to benefit from incentive fee structures.

- The Regulatory and Training Runway Is Short. With FAR amendments due within 120 days and agency-level guidance from OMB within 45 days, the policy changes will begin taking effect quickly. Contractors should monitor the Federal Register closely, engage their agency contracting officers proactively, and begin internal assessments of how their existing and pipeline contracts may be affected.

What About Better Requirements From Agencies?

The ongoing push for increased economies and performance by contractors is not without its merits. Most people understand the concept of value and timeliness in making purchases. However, the other side of the equation that must be addressed and has contributed to the use of (dare I say, need for?) Cost+ and other flexible contracting models is the quality of contract requirements developed and sustained by the agencies seeking solutions from industry. Too often, we read and hear of solicitations bearing requirements that are less than precise, difficult to measure, or change over time. To successfully meet expectations requires well-defined targets. No surprise there.

If agencies require flexibility to adapt to changing circumstances or evolving technologies, then there is a cost to bear in that. Expecting contractors to build these flexibility costs into fixed- or performance-based contracts may have the net effect of raising the cost of those contracts.

Final Thoughts

The latest EO dovetails with a recent OMB memorandum pressuring agencies to shift from custom solutions to commercial offerings, continuing OMB’s drive for cost-savings. These efforts run in parallel to OMB’s drive for greater transparency and visibility in federal contracting through the sharing of contractor pricing data among agencies.

As we approach the half-way mark of the second Trump Administration, the pace and scope of their acquisition reform agenda shows little sign of slowing. Contractors will need to remain diligent to keep up with the pace of change or risk losing their edge in this increasingly competitive market.