Nearly 25% of Yearly Defense IT Dollars Get Spent in September – Are you ready?

Published: August 20, 2013

USAFARMYDEFENSEDISAForecasts and SpendingNAVY

There’s just another two weeks before the traditional federal IT busy season goes into its customary hyper-drive reserved for the final month of the fiscal year – September. And with it the Department of Defense will likely obligate nearly 25% of its fiscal year (FY) 2013 IT funds, all within a single month. So how much are we talking about and where is it likely to go?

In a previous entry, I drew attention to the fact that of the more than $380 billion in reported IT obligation over the last 5 years from FY 2008 through FY 2012, nearly 40% comes in Q4 each year and 23% comes in September alone. That translates into an average of over $17 billion in IT obligations in each September. This week, I want to zero in on the Defense sector of the federal IT market.

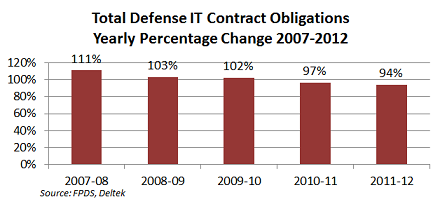

Historically, the Defense portion of the federal IT market has seen consistent spending growth. But like the overall market, the Defense IT sector has softened a bit in the last few years. Instead of the year-over-year growth in IT contract obligations that we saw as recent as FY 2009-2010, the last two years have seen overall drops from the previous year. (See chart below.)

The dollars of reported IT obligations behind the yearly negative change rates for the last few fiscal years, 2010-2012 are $50.0 billion, $48.3 billion, and $45.5 billion respectively. If we assume the downward trend continues and arbitrarily select the most recent 94% yearly change and apply it from FY 2012 to FY 2013 we arrive at a ball-park estimate of roughly $42.9 billion for FY 2013, which ends at the end of September. (See chart below.)

September is Big in Defense IT

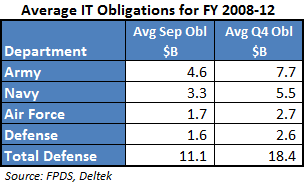

Let’s turn our attention to the fourth fiscal quarter (Q4) and September in particular. Taking the aggregate 5-year obligations and the percentage of this spending that fell in Q4 – and in September in particular – reveals that over the last 5 fiscal years, FY 2008 – FY 2012, the Navy and Army obligated an average of 40% of their yearly IT spending in Q4. The Defense agencies and Air Force are not far behind at roughly 35%. Further, each of these branches obligated from 20-24% in the month of September, on average, during the same period. (See chart below.)

Bringing it back to dollars, over the last five years Defense sector reported an average of over $18 billion in IT obligations in Q4 and an average of more than $11 billion in the final month of the fiscal year. (See table below.) If we keep with the 94% rate for FY 2013 used above we could be looking at an FY 2013 Q4 Defense IT spend of more than $17 billion – with September alone reaching $10 billion.

What Are They Buying?

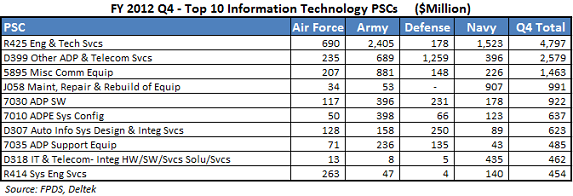

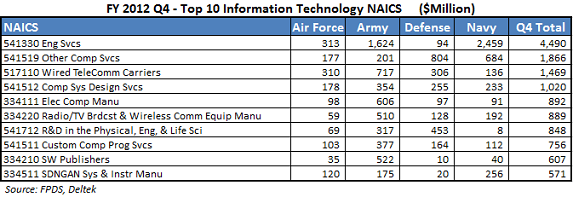

What can we tell about what the Defense Department may be buying during this Q4 spending spree? The most granular data we have is by the Product Service Code (PSC) and North American Industry Classification System (NAICS) code reported on the prime contract obligation. Below are the top 10 PSCs and NAICS based on their total reported Q4 obligations for the most recent completed fiscal year 2012.

The mix of service and product categories gives us a sense of where most of the Q4 dollars were bucketed in FY 2012. These 10 PSCs each account for $13.4 billion of the $17.8 billion (75%) Defense IT obligations reported in Q4 of FY 2012. The NAICS proportions are effectively the same 75% as it turns out.

Granted looking at the data tagged to these classification codes has its limitations since only one primary code can be used for each classification scheme on a reported prime contract. This means that a significant amount of secondary elements like software and/or hardware purchases that are purchased as part of larger solutions contracts get reported under a services code, obscuring them from visibility. Also, since these are all prime contract dollars, we have no visibility into any related subcontracts and/or teaming partner companies that may receive a portion of this funding. That said, it is the best data we have available and it does give us a sense of volume and proportionality.

Implications

By several accounts, the $43 billion “back-of-envelope” guestimate of total Defense IT obligations for FY 2013 may be optimistic. Depending on who you talk to attitudes about this year’s federal busy season range from cautious optimism to downright gloom – a range that we are not accustomed to seeing in the federal IT market. With the outlook for FY 2014 at this point decidedly pessimistic some see DoD working to find ways to squirrel away funds from this year to help ease the pain next year. Yet, we are seeing some reports of contracts getting awarded with FY 2013 funds, so it is still unclear whether such pessimism is warranted.

Even if there turns out to be cuts in overall FY 2013 IT spending that buck historical spending levels, that does not negate the Q4 spending trend that has become ensconced over the last decade or more. That means that whatever agencies have left to spend of expiring 2013 funds will be looking for an outlet. And now that the Pentagon has reduced sequestration-related furloughs of civilian employees, DoD IT acquisitions shops that depend on these people should be able to handle the volume. Firms with the right contract vehicles in place and solutions offerings that fall under these PSC/NAICS classifications stand best positioned to win this end of year business.