After a Strong FY 2025, Defense and Aerospace Contracting is Poised for Future Growth

Published: January 15, 2026

Federal Market AnalysisContracting TrendsDEFENSEDefense & AerospaceForecasts and SpendingDHSNASASpending TrendsDOT

Defense and Aerospace contracting posted a record year in FY 2025, and indications are that the trend could continue.

Recently, I wrote about reasons to be optimistic about the state of the federal contracting market, based on how strongly the market finished out fiscal year (FY) 2025 – especially in Q4 – and how Q1 of FY 2026 has begun reasonably well, even with the government shutdown inaugurating the new fiscal year.

Today, I will unpack the contracting data a bit more to see what broad areas may present the brightest opportunities as we progress through FY 2026. Spoiler alert: it is Defense and Aerospace.

Strong Federal Spending in FY 2025 Favored a Few Key Areas

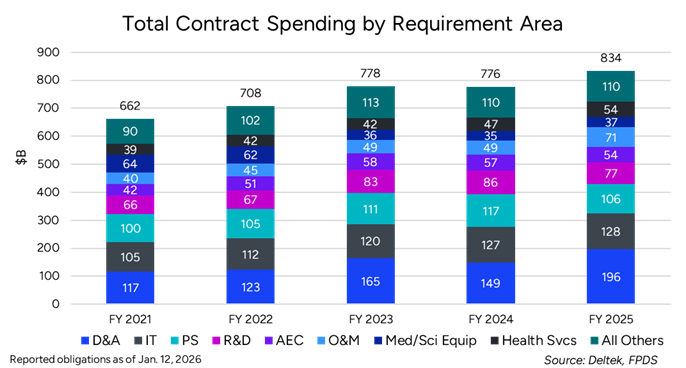

Even with the many changes and uncertainties that came throughout the year, FY 2025 came in as a new record high for federal contract spending, with total contract spending growing by $57.4B (+7.4%) to reach $834B across all areas.

As is typical, not every area of contracting saw year-over-year growth from FY 2024. The largest eight primary contract requirement categories that accounted for more than 85% of total federal contacting dollars in FY 2025 were a mixed bag of winners and losers.

From a growth perspective, FY 2025 favored Trump Administration priorities around national defense and healthcare services. The fiscal year saw the following growth/reduction of these primary contract requirement areas:

- Defense & Aerospace (D&A): +$47.4B (+32%)

- Information Technology (IT): +1.0B (+1%)

- Professional Services (PS): -$11.2B (-10%)

- Research & Development (R&D): -$9.0B (-11%)

- Architecture Engineering and Construction (AEC): -$2.9B (-5%)

- Operations & Maintenance (O&M): +$23.0B (+47%) – Note: See discussion below.

- Medical & Scientific Equipment (Med/Sci Equip): $2.0B (+6%)

- Health Services (Health Svcs): +$6.9B (+15%)

- All Other Categories: $113M (+0.1%)

Looking at the relative proportions that these contract requirements represent across total spending in FY 2025, D&A and O&M accounted for a historically disproportionate level of federal contracting, compared to the last four years.

I will look at the D&A spending below, but first I want to address an observation about the growth in O&M in FY 2025. When looking deeper into the data, the O&M bucket is highly influenced by a contract reporting issue by the government, specifically, the State Department.

State reported nearly $22.7B in O&M obligations for September 2025, the final month of fiscal year, for eight awards under their Facilities O&M Services IDIQ contract. That accounts for nearly all the $23.0B in O&M growth for all of FY 2025. Then, in December (i.e., in Q1 FY26), State de-obligated all but $70.8K of that amount, issuing a modification to correct a reporting error where the ceiling value of the eight awards was also entered as action obligations on those awards, thus inflating the O&M bucket greatly. (For more details, see GovWin IQ opportunity ID # 249601.)

The point here is that we are working with the data that is provided by government agencies, and so some of this data is open to agency revision. GovWin diligently monitors, updates and fully discloses this information as we become aware of it.

Also, I highlighted some observations about the Information Technology (IT) and Professional Services segments in a previous article, so check that out for those areas.

Defense and Aerospace Drove Market-wide Contracting Growth in FY 2025

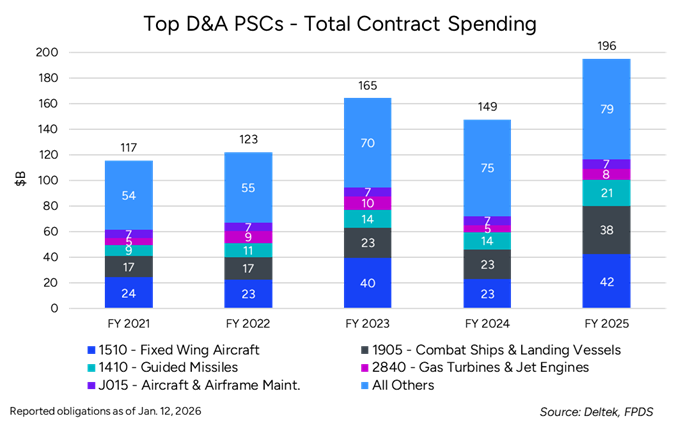

Of the $57.4B in total contracting growth in FY 2025 noted above, D&A contract spending alone accounted for $47.4B, nearly 83%. Nearly $44.5B of that growth came from contracts listed under five Produce and Service Codes (PSCs) among the 100 PSCs reported on D&A contracts over the five-year period.

From FY 2024 to FY 2025, these top five PSCs grew strongly or sustained their spending position, reflecting current administration priorities:

- 1510 - Fixed Wing Aircraft: +$19.3B (+84%)

- 1905 - Combat Ships & Landing Vessels: +$14.6B (+64%)

- 1410 - Guided Missiles: +$7.1B (+53%)

- 2840 - Gas Turbines & Jet Engines: +$3.1B (+59%)

- J015 - Aircraft & Airframe Component Maintenance: +$280M (+4%)

- All Other D&A PSCs: +$3.1B (+4%), including:

- 1425 - Guided Missile Systems, Complete: $5.2B in FY25, +$1.2B (+30%)

- 1420 - Guided Missile Components: $4.0B in FY25, +$407M (+11%)

These top five PSCs accounted for 60% of D&A contract spending in FY 2025, which is a higher proportion than recent fiscal years.

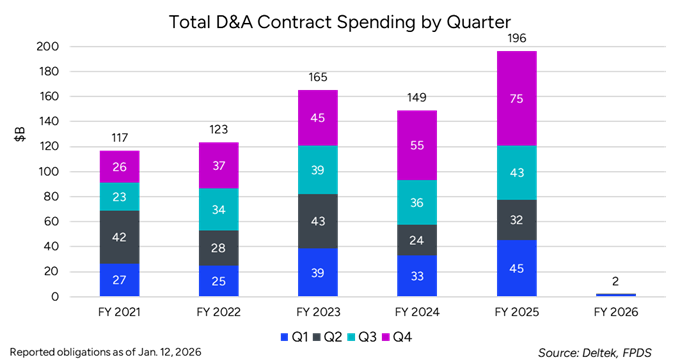

Looking forward to potential D&A growth in FY 2026 and beyond, the following chart provides a breakout of how D&A contract spending has occurred among fiscal quarters over the last five complete fiscal years. FY 2026 is underreported so far, due to the traditional Department of Defense (DoD) 90-day lag in reporting, so it will take a few months to get a true picture.

Over the last five years, more than 75% of total yearly D&A spending has come in Q2-4, so if FY 2026 spending follows that pattern then there is plenty of contract opportunity yet to come in 2026.

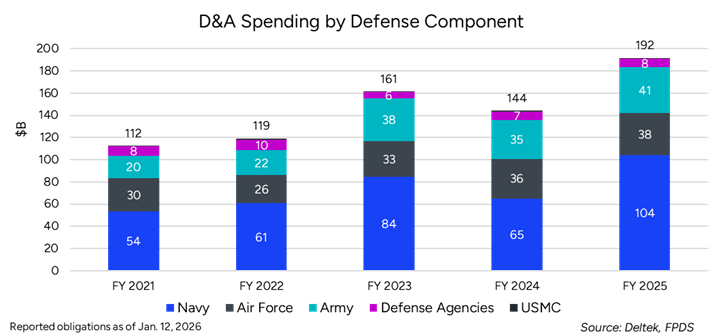

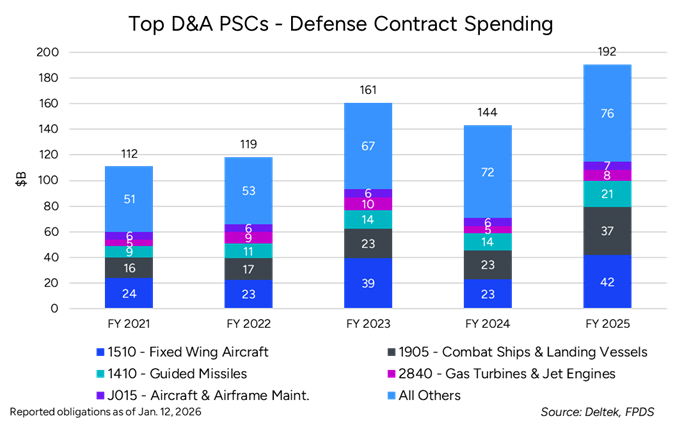

Defense and Aerospace Contracting by the Department of Defense (DoD)

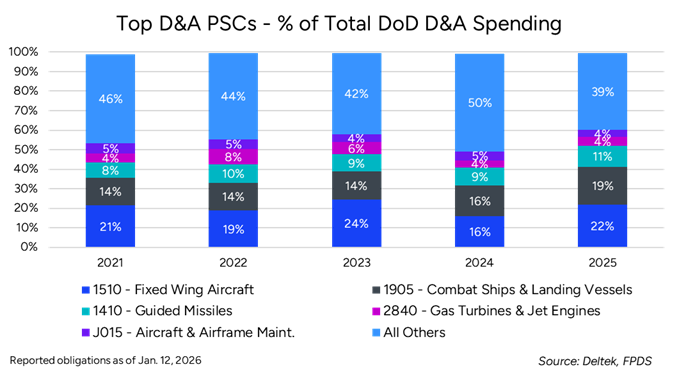

It is no surprise that D&A spending would dominate among DoD contract requirement categories, and at $192B in FY 2025 that DoD D&A would account for nearly 89% of government-wide D&A spending for the year. Further, D&A accounted for 37% of all Defense Department contract spending in FY 2025, up from 30% in FY 2024 and 33% in FY 2023.

Other FY 2025 growth areas among the largest categories were Medical & Scientific Equipment (+$1.6B, +15%), Machinery, Equipment & Tools (+$1.3B, +7%), and IT (+$2.7B, +4%). Even Professional Services – an area for targeted spending reductions by the administration – held steady in FY 2025 with $592M (+1%) in growth from FY 2024. On the downside, R&D and Architecture Engineering and Construction (AEC) saw year-to-year reductions of -$5.0B (-8%) and -$4.7B (-12%), respectively, but the spending levels in those categories are still not wildly outside the recent historical levels.

Every DoD component reported D&A spending growth in FY 2025, after most components had reductions or relatively modest increases from FY 2023 to FY 2024.

Given the DoD’s dominance in D&A contract spending, it is no surprise that the top D&A PSCs among Defense components mirror those at the market-wide level, accounting for an aggregate $115B in D&A contract spending at the DoD in FY 2025.

Total DoD D&A contracting grew from FY 2024 to FY 2025 by $47.5B (+33%), and these top five D&A PSCs accounted for $44.2B, or 93%, of that growth.

Taken together, these top five PSCs have risen in proportion of total DoD D&A spending from 54% in FY 2021 to 61% in FY 2025.

At this point in the Trump Administration, it is likely that spending around these priority areas will be sustained into the current fiscal year and potentially after.

Defense and Aerospace Contracting by Civilian Agencies

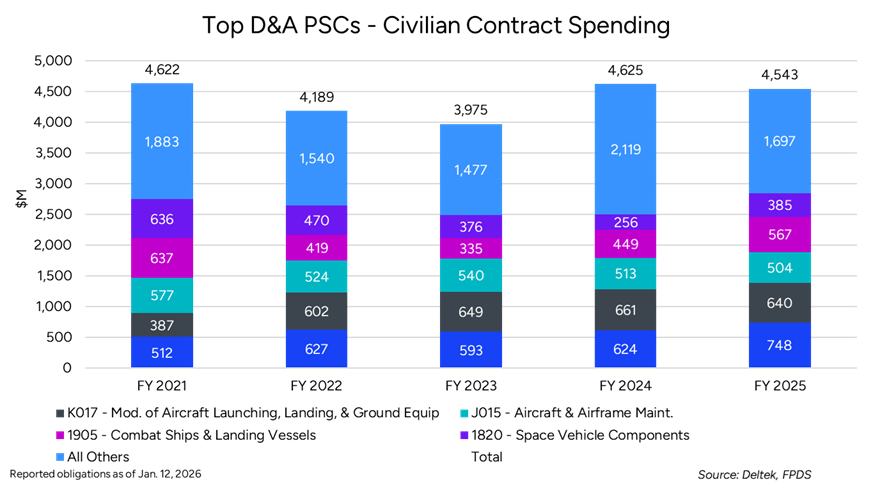

As one might expect, D&A contract spending by Civilian agencies is considerably less than Defense. Overall, Civilian agencies spent about $4.5B on D&A contracts in FY 2025, which is down about 2% from FY 2024, but was a significant rebound from FY 2023.

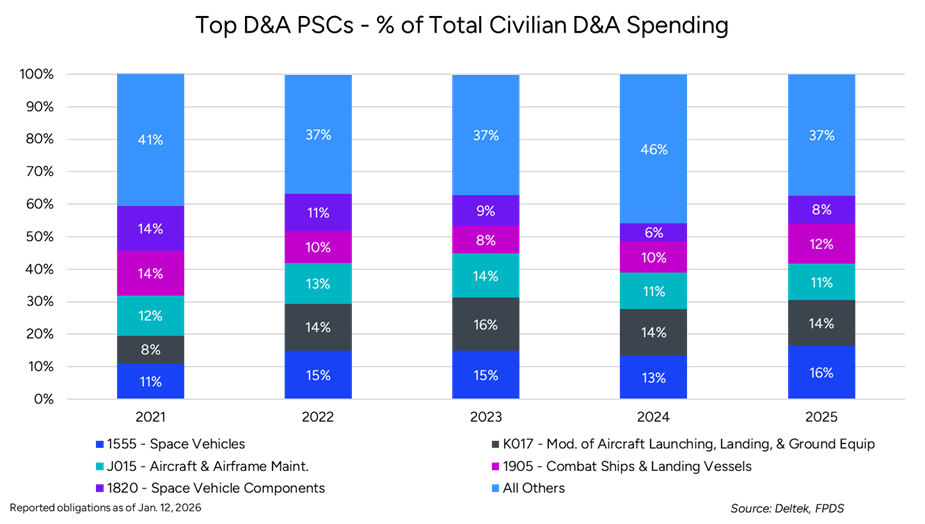

The top Civilian D&A contract spending agencies – the National Aeronautics And Space Administration (NASA), and the Departments of Homeland Security (DHS), Transportation (DOT), State, Commerce (DOC) and Justice (DOJ) – have accounted for 96-98% of Civilian sector D&A contracting over the last five fiscal years, beginning on the lower end in FY21 and growing to 98% in FY 2025.

NASA, DHS and DOT D&A contracting grew from FY 2024 to FY 2025, whereas State, DOC and DOJ saw significant reductions, driven by changing administration priorities. However, all six of these entities reported sizeable growth in D&A spending from FY 2023 to FY 2024, so the multi-year growth trend for NASA, DHS and DOT is noteworthy.

Here are the FY24-25 changes for each agency:

- NASA: +$54M (+4%)

- DHS: +$304M (+25%)

- DOT: +$85M (+11%)

- State: -$157M (-37%)

- DOC: -$350M (-76%)

- DOJ: -$20M (-14%)

- All Others: +$2.2M (+2%)

Narrowing the focus onto specific PSCs in the Civilian sector, of the total $4.5B in Civilian D&A spending in FY 2025, the top five D&A PSCs accounted for $2.8B (63%) of that total, which is roughly on par with the DoD’s top five proportion.

Naturally, the Civilian agencies have a slightly different mix of top PSCs from the DoD, and the occurrence of the two space-related PSCs, which accounted for 25% of Civilian D&A spending in FY 2025, shows NASA’s prominence in this contracting area.

Not all the top five Civilian D&A PSCs experienced growth from FY 2024 to FY 2025:

- 1555 - Space Vehicles: +$124M (+20%)

- K017 - Mod. of Aircraft Launching, Landing, & Ground Equipment: -$21M (-3%)

- J015 - Aircraft & Airframe Maintenance: -$9MB (-2%)

- 1905 - Combat Ships & Landing Vessels: +$118M (+26%)

- 1820 - Space Vehicle Components: +$130MB (+51%)

- All Others: -$422M (-20%)

Taken together, these top five PSCs have maintained a steady proportion of total Civilian D&A spending over the period – about 63% – except for FY 2024, which saw them fall to 54% of total spending.

Defense and Aerospace D&A Growth at NASA, Homeland Security and Transportation

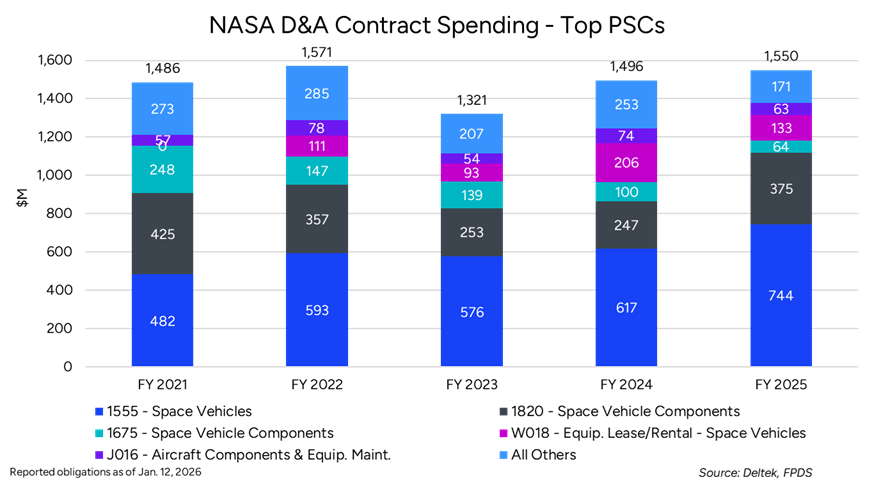

The top three Civilian agencies that showed D&A spending growth in FY 2025 were NASA, DHS and DOT. While the National Aeronautics and Space Administration grew in FY 2025, the $1.5B in spending was relatively in line with previous years, so from a growth perspective the greater opportunity has been at DHS and DOT.

In FY 2025 the 1555 - Space Vehicles PSC experienced $127M (+21%) in growth, sustaining the $41M (+7%) growth that it had in FY 2024. The only other top D&A PSC that saw growth in FY 2025 was 1820 - Space Vehicle Components at +$129M (+52%). Most of the remaining top PSCs saw reductions in FY 2025 after seeing a boost in FY 2024.

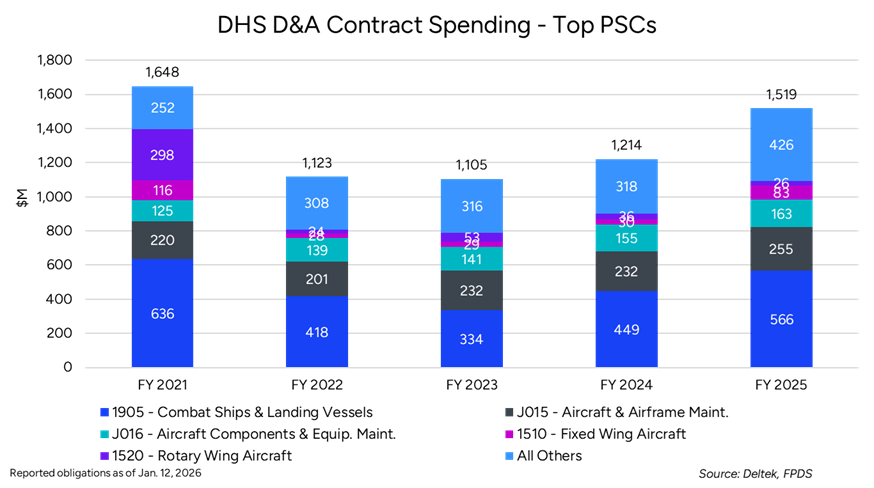

At the Department of Homeland Security, D&A spending has been on a significant rebound, especially in FY 2025. Each of the top five D&A PSCs have enjoyed multi-year growth since FY 2023, except for 1520 - Rotary Wing Aircraft. In fact, each of the four other top PCSs have experienced double digit percentage growth since 2023.

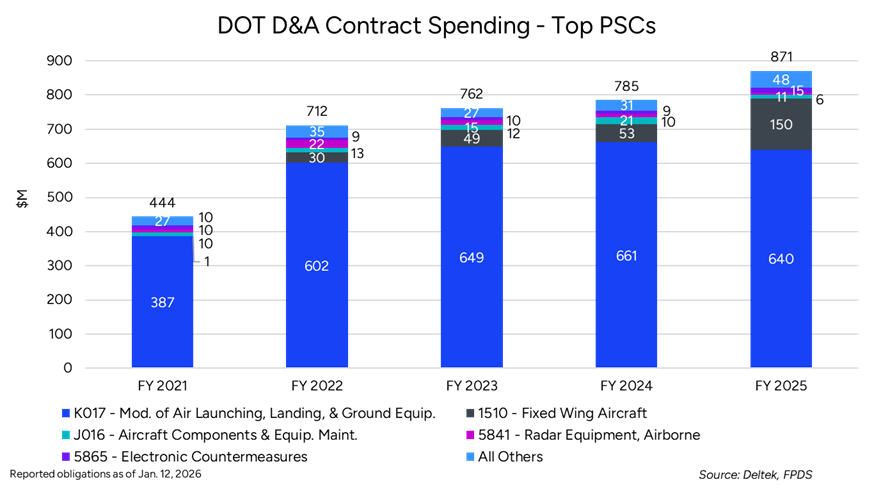

The Department of Transportation D&A contract spending is overwhelmingly dominated by PSC K017 - Modification Of Equipment- Aircraft Launching, Landing, And Ground Handling Equipment, which historically accounts for roughly 85% of DOT D&A contact spending. However, in FY 2025, 1510 - Fixed Wing Aircraft jumped by nearly $97M (+182%).

Future Opportunities

While FY 2025 saw more than its share of change, the year provided some growth opportunities in federal contracting, especially in the Defense and Aerospace areas supporting Trump Administration national defense and security priorities.

From most indications, it appears that Congress is likely to continue funding these priorities throughout FY 2026 and beyond, signaling the potential for sustained contract opportunities in these areas. While the administration continues to increase its scrutiny of D&A company contract performance, those that perform well will continue to reap the benefits of participation in this critical market segment.